Buffet’s Math Trumped by Gold

By: Roy Sebag

Introduction

Every year, I patiently await the release of Warren Buffet’s Annual Letter written to shareholders of Berkshire Hathaway. Though I have “evolved” when it comes to macroeconomics and my understanding of monetary history, I still consider myself first and foremost a bottom-up deep value investor and view this methodology as the only logical method to analyze, invest, or short securities traded by market participants in a free market. As far as value investors go, Buffet and his mentor Benjamin Graham are not only the best practitioners of the craft but have basically re-invented it and evangelized it. For that, every investor should have and maintain great respect for Warren Buffet, Benjamin Graham and others including Charlie Munger, Irving Khan, Walter Schloss, and David Gottesman.

Value investing is what led Buffett to become the greatest investor of all time. He has, through his initial understanding of value investing, accumulated a collection of nearly 300 businesses spanning the globe. He has also amassed a significant fortune and more importantly, power. The same goes for Charlie Munger. With that power also comes an undoubted level of hubris, patriotism, and dare I say, statism.

Anyone that has followed the two as closely as I have can point to the specific moment when both realized their position of power was far more important to their interests than their ability to deduce market and political behaviour based on logic. It was 2008 when the financial crisis hit. That was when I believe Buffett and Munger realized they had become so successful and so big while the rest of the financial sector was so indebted and insolvent that, unless they started cheerleading, everything they had built would also be lost. It was ultimately fear which led Buffet to support Hank Paulson and even the big banks in stark contrast to his public positions in the prior decade.

I wrote about this in depth in an essay from 2012 which is entitled: “Respectfully Disagreeing with Buffett’s Recent Views on Gold”. I found it difficult to reconcile Buffett’s unsolicited comments about gold with the empirical historical data relating to his investment in silver, his public comments about inflation, and his father’s deep comprehension and support of the gold-standard as a congressman. Later this year, I will also dismantle Buffet’s comment to Becky Quick on CNBC by demonstrating that gold has actually outperformed the Dow. That piece will show that there has not been any investment vehicle that would have enabled an investor to mirror the performance of the Dow index.

In short, reaching this stage has required a deep understanding of value investing, Berkshire Hathaway’s history, and gold to disprove these arguments, and I am grateful to possess this multidisciplinary approach.

Buffett’s Latest Rhetoric

In Buffett’s 2015 Annual Letter, sandwiched between a logical review of the company’s achievements, is Buffett’s latest attempt to cheerlead and obfuscate. Unfortunately for Buffett, I had nothing to do this weekend and decided to put together a point by point rebuttal to his latest rhetoric and sophistry.

On page 7 of the annual letter, Buffet writes the following:

It’s an election year, and candidates can’t stop speaking about our country’s problems (which, of course, only they can solve). As a result of this negative drumbeat, many Americans now believe that their children will not live as well as they themselves do.

That view is dead wrong: The babies being born in America today are the luckiest crop in history. American GDP per capita is now about $56,000. As I mentioned last year that – in real terms – is a staggering six times the amount in 1930, the year I was born, a leap far beyond the wildest dreams of my parents or their contemporaries. U.S. citizens are not intrinsically more intelligent today, nor do they work harder than did Americans in 1930. Rather, they work far more efficiently and thereby produce far more. This all-powerful trend is certain to continue: America’s economic magic remains alive and well. [emphasis added]

Here Buffett is obviously taking a jab at politicians and other market participants that state the obvious: The US and other western economies are slowing, labor participation rates are at an all-time low, fertility rates are declining, household formation rates are declining, inflation is rising in the things we need, deflation is creeping in the things we own and most importantly, the gap in wealth inequality keeps growing to unprecedented levels.

These statements are not hypotheses; they are empirical and point toward a deviation from the historical path which made western democracies such as the US the most impressive prosperity machines in history. Buffett is once again fearful as he was in 2008 because he knows very well that the solution to recalibrating the path is the aggressive revaluation of the ratio of global assets to global debt.

Buffet’s creative solution is to leverage his deep understanding of real-inflation which forms the crux of his insurance float business model to obfuscate US data and convince readers that Americans are better off today than they were in 1930 (the year Buffett was born). He elects US GDP per Capita as the metric to convey this view and authoritatively declares that everyone else is “dead wrong”.

“Real” GDP per Capita – Many ways to Skin the Cat

Buffett arrives at a $56,000 2016 “Real” GDP per Capita for the US. He does so by saying “about $56,000”. Now, I could not reconcile this figure, the closest I came was via the St. Louis Fed’s “Real Gross Domestic Product per Capita” figure published here which comes in at $50,993 for Q4 2015. Nevertheless, let us take Buffett’s $56,000 figure at face value.

The Real GDP per Capita is calculated by taking the nominal GDP in US Dollars (which we have a history of dating back to 1790) and dividing that figure each year by the population figures. The result is a nominal GDP per capita figure one can trace back to 1790. A good website for perusing this type of data is: www.measuringworth.com. Here is where the monkey magic begins. Economists and now Buffet take this nominal data which is empirical and deflate it with some type of a formula to arrive at what they consider the “real” GDP per Capita figure. This, they claim provides an accurate measurement of historical GDP per Capita figures in today’s unit of account and helps to measure productivity over time.

Of course, any intelligent market participant knows the formula used by most economists (the consumer price index) is severely flawed and doesn’t reconcile with reality. Recently, I published a short piece on ZeroHedge showing how the Economist magazine uses the CPI and other useless formulas to manipulate gold’s true performance.

GDP per Capita Priced in Gold

When it comes to financial analysis, I try and focus on what I consider to be “universal truths”: wisdom or knowledge that is as close to foundational as possible. Mathematics for example, is universally true. Gravitational forces in the universe are also universally true. Buffett’s analysis and conclusion lacks rigor as it relies on a subjective variable (deflating a historical nominal GDP by a CPI index to measure productivity and quality of life) and then disregards the most important one: That 20.67 US Dollars in 1930 was equivalent to 1 Troy Ounce of .9999 or better elemental Gold (Au).

Buffett makes the argument that his $56,000 today is six times better (even after his adjustment for inflation) than the $858 of GDP per Capita each US Citizen earned in 1929 but forgets to mention that $858 in 1929 was equivalent to 41.5 Troy Ounces of Gold in 1929. Here is the math:

The result is unequivocal: When measuring on an apple to apples comparison, there has been little to no gain in GDP per capita over the last 86 years in the United States. There is most certainly not a six times increase in productivity nor is there an increase in the quality of life per capita as measured using the same unit of account that was used in 1929. Buffet’s manipulating of the figures without reconciling under the apple to apples gold method is trumped by math.

I have built a graph of US GDP per Capita priced in Gold from 1929 to 2015. On first glance, this graph appears to show that there were in fact times where, as measured on an apple to apples basis, the US was gaining in both productivity and quality of life on a per capita basis.

A part of me agrees with the graph and ascribes the first cycle from 1942 to 1971 as a classic post-war expansion fueled by healthy demographics, sound economic policies, normalized interest rates and the discovery and proliferation of conventional oil as a primary energy source. The second period from 1987 to 2001, in my view reflects the Greenspan era of targeting the gold price with the fed funds rate as he explains in his book “Age of Turbulence”. Though there were many unintended consequences brewing, market observers should agree that interest rates from the early 1980’s to 2001 incentivized savings and productive usage of capital.

Today, we have neither. We don’t have a market rate that incentivizes savings, nor do we have healthy demographics or sound economic policies. Most millennials prefer to remain single and defer household formation. When they do form households, their fertility rates are far lower than their parents.

GDP per Capita Priced in Gold Excluding Government Spending

There is an even more distressing analysis of the GDP per capita figures. In searching through the data, I noticed that government spending as a percentage of nominal GDP has been creeping up from 1930’s through today. If one is to extrapolate productivity or quality of life from GDP per capita as Buffet has done, shouldn’t the government component be excluded? Even the most ardent Keynesian would agree that government spending is not the arbiter of the free market but there to smoothen out the business cycle.

In 1929, government spending as a percentage of GDP was 11.16%. In 2015, it was 36%. Unsurprisingly, the adjustment of nominal GDP each year to exclude government and the subsequent adjustment of the resultant figure to Gold from 1929 to 2015 shows a completely different picture:

Though this graph resembles the prior graph, it’s important to observe carefully. The Gold adjusted Ex Gov Spending GDP per Capita figure shows less pronounced cycles than before. This is crucial as it indicates a longer-term asymptotic decline in peaks achieved by the US economy when excluding government spending. For market participants familiar with technical analysis, this resembles a “lower high” chart pattern. More importantly, the 2015 Gold adjusted Ex Gov Spending GDP per Capita figure is $35,690 down 17.3% over 86 years vs. $43,157 which was the same figure for 1929.

Conclusion

We cannot prosper as a society unless we are using the right measurement tools. In this piece I showed how Warren Buffet was able to fool most people into believing they are six times better off today than their ancestors. It’s easy to convince anyone of anything if the author is both brilliant, powerful, and has an artifice through which they can distort the past. By using a measurement tool that is totally arbitrary such as the CPI to deflate nominal GDP per Capita, Buffett attempts to show empirical and logical analysis.

In reality, he diverted the public’s attention from a critical factor: that the historical dollars were redeemable in gold.

If you understand basic science and elementary physics, you will quickly grasp why only gold should be used as a measuring system for our productivity and prosperity. Most people who own gold don’t fully understand why they do. In my encounters with leading gold investors and market participants, the smartest own it because they understand it to be antithetical to everything else in financial markets. Another popular axiom is: It’s an “asset” without counterparty risk or an “insurance policy”. These are reasons for owning gold that miss the critical reason for why gold ascended as money in the first place. For those interested, I recommend these two pieces. The answer has little to do with economics and lots to do with physics:

Why Gold – BitGold.com by Roy Sebag and Josh Crumb

Gold Price Framework Vol. 1: Price Model by Stefan Wieler and Josh Crumb

At GoldMoney Inc. (TSX: XAU.V), we continue to build the world’s first full-reserve and gold-based financial services company offering savings, payments, wealth services, custody, execution, and research for nearly 750,000 clients in 200 countries. By doing so, we empower people around the world to measure their prosperity with something remarkable and timeless.

First published here: http://www.zerohedge.com/news/2016-02-29/buffet%E2%80%99s-math-trumped-gold

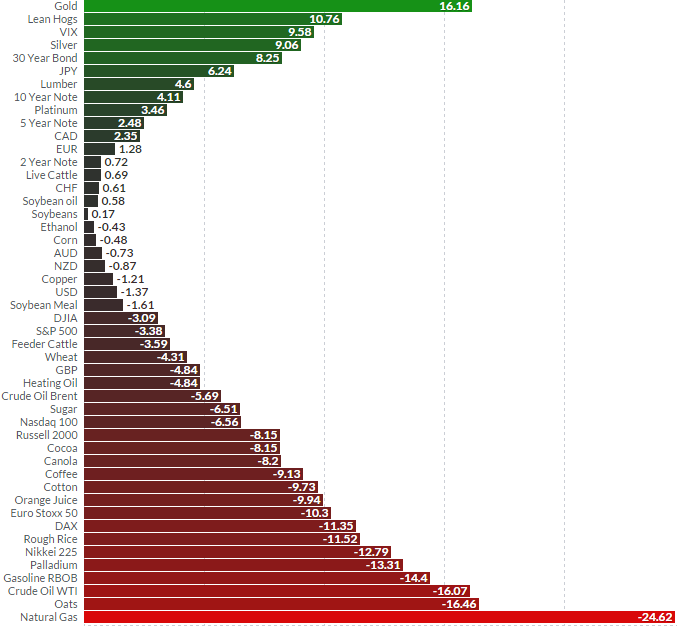

Market Performance in February – Finviz.com

Market Performance in February – Finviz.com

Gold and silver prices are being driven higher by global economic weakness and the growing number of central banks implementing negative interest rates. While gold and silver prices normally have a negative relationship to a strong U.S. dollar and low interest rates, that’s not the case this time around. And until the global economy registers sustainable growth, gold and silver will continue to be one of the most attractive investments out there.

Gold and silver prices are being driven higher by global economic weakness and the growing number of central banks implementing negative interest rates. While gold and silver prices normally have a negative relationship to a strong U.S. dollar and low interest rates, that’s not the case this time around. And until the global economy registers sustainable growth, gold and silver will continue to be one of the most attractive investments out there.

Here’s Why Silver Prices Could Soar 800%

Here’s Why Silver Prices Could Soar 800%